0% APR Business Cards: The Best Options for Startup Cash Flow in 2026

Every founder knows the moment.

You need to invest in growth—but your bank balance says “slow down.”

Business credit card interest rates averaged 21.5% in 2025. On a $10,000 balance carried for a year, that’s $2,150 in interest alone—money that could have hired a part-time intern or bought inventory. [citation:4]

That’s why smart founders don’t just look for credit cards.

They look for 0% APR windows—temporary financing tools that can stretch cash flow without immediate interest.

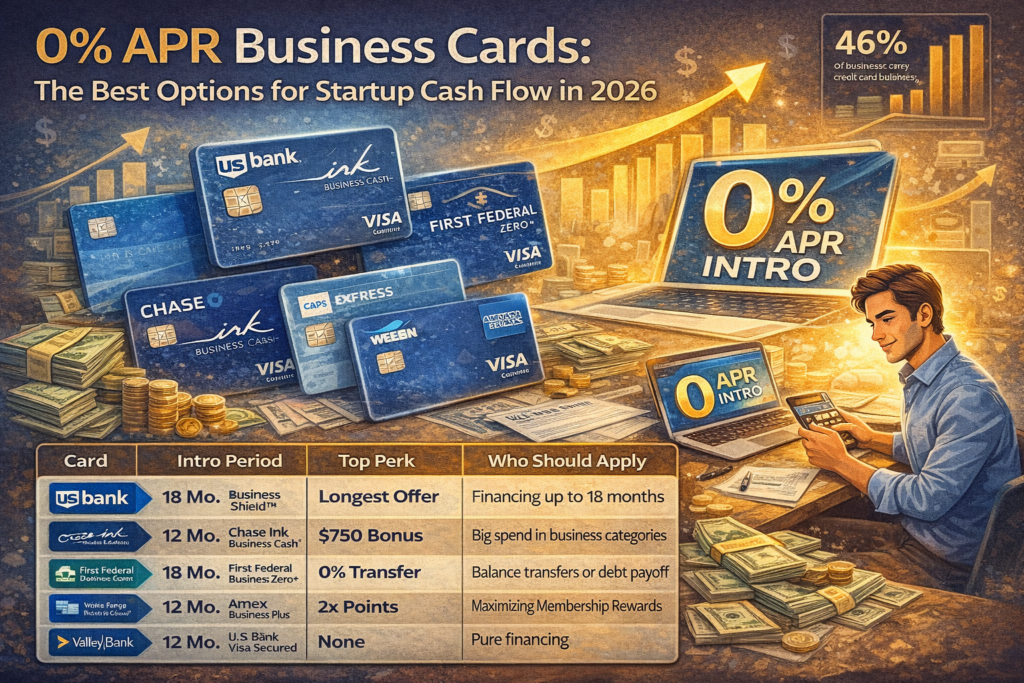

In fact, 46% of businesses carry month-to-month credit card balances, risking escalating interest costs that eat into margins. [citation:4]

Used correctly, a 0% intro APR card is not “free money.”

It’s working capital with a deadline.

0% Intro APR vs. No-APR Charge Cards: Not the Same Thing

Many founders confuse these two. They shouldn’t.

| Feature | 0% Intro APR Card | No-APR Charge Card |

|---|---|---|

| How it works | 0% interest for 6–18 months, then variable APR (15–29%) | Balance must be paid in full monthly |

| Carry a balance | Allowed during intro period | Not allowed |

| Ideal for | Big purchases, seasonal cash flow | Recurring expenses, predictable revenue |

| Credit score needed | Usually 670+ | Often revenue-based approval |

| Examples (2026) | Chase Ink, U.S. Bank Business Shield, First Federal Zero+ | Brex, Ramp |

Sources: [citation:4][citation:6][citation:7]

Translation:

- 0% APR cards = temporary financing tools.

- Charge cards = spending tools with no interest because there’s no debt.

The Best 0% APR Business Cards for Startups in 2026

Here are the top options available right now.

| Card | Intro APR | Duration | Bonus | Rewards | After Intro | Best For |

|---|---|---|---|---|---|---|

| U.S. Bank Business Shield™ Visa® | Purchases + transfers | 18 months (branch) / 12 online | Not specified | 5% travel portal + $50 annual credit | Standard variable APR | Longest intro period [citation:1] |

| Chase Ink Business Cash® | Purchases | 12 months | $750 after $6k spend | 5% office/telecom, 2% gas/restaurants | Variable APR | High bonus + business categories [citation:2][citation:3] |

| First Federal Business Zero+ | Purchases + transfers | 18 months | Not listed | 5% travel portal | Variable APR | Long balance transfers [citation:5] |

| Amex Blue Business Plus™ | Purchases | 12 months | 15k points | 2x points up to $50k/year | Variable APR | Flexible points [citation:3][citation:7] |

| Amex Blue Business Cash™ | Purchases | 12 months | $250 bonus | 2% cash back up to $50k/year | Variable APR | Simple cash back [citation:3][citation:7] |

| Wells Fargo Signify Business Cash® | Purchases | 12 months | $500 bonus | 1.5% flat cash back | Variable APR | Existing Wells Fargo clients [citation:3][citation:6] |

| U.S. Bank Business Platinum | Purchases + transfers | 12 months | None | None | Variable APR | Pure financing [citation:6] |

| Valley Bank Visa Secured | Purchases | 6 months | None | 1% cash back | Variable APR | Limited or poor credit [citation:6] |

The 18-Month Club: Cards That Give You More Time

In 2026, 18 months is the new gold standard for startup financing.

Two cards dominate this category:

U.S. Bank Business Shield™ Visa®

- 18 billing cycles at 0% APR (branch application)

- One of the longest intro offers available in 2026. [citation:1]

First Federal Business Zero+

- 18 months on both purchases and balance transfers

- Currently the longest combined offer on the market. [citation:5]

Why this matters:

If you finance $10,000:

- 12-month intro = $833/month payoff

- 18-month intro = $556/month payoff

That’s a 33% lower monthly cash burden.

The Charge Card Alternative: When 0% APR Isn’t the Answer

Not every startup should carry balances.

Some businesses have:

- Predictable revenue

- High recurring expenses

- Strong monthly cash flow

For them, charge cards make more sense.

Brex

- No personal credit check

- Approval based on revenue

- Rewards in tech, travel, and SaaS categories [citation:6]

Ramp

- 1%–1.5% flat cash back

- Approves businesses with limited or poor credit

- No interest because balances are paid monthly [citation:4][citation:5]

Who charge cards are best for

- SaaS companies

- Agencies

- Subscription-based businesses

- Any startup with predictable monthly revenue

These companies don’t need financing.

They need spending tools and rewards.

How Much Should You Finance? The Monthly Payment Calculator

Before using a 0% APR card, calculate your payoff plan.

Examples:

- $5,000 over 9 months = $556/month

- $5,000 over 12 months = $417/month

- $10,000 over 18 months = $556/month

[citation:7]

Simple formula

(Total purchase ÷ intro months) + safety margin

Example:

$8,000 over 12 months:

- $8,000 ÷ 12 = $667/month

- Add $50 buffer

- Target payment: $717/month

This prevents last-minute interest charges.

Stacking Cards for Maximum Runway

Advanced founders rarely use just one card.

They build a financing stack.

Strategy example

Card 1: 0% APR

- Use for inventory or equipment

- 12–18 months of free financing

Card 2: Charge card

- Use for:

- SaaS

- Ads

- Cloud services

- Earn rewards on operating expenses

Card 3: Second 0% APR

- Open 12 months later

- Extend interest-free runway

This creates a rolling credit runway without interest.

The Trap of the “Free Money” Illusion

Here’s the psychological risk.

Research cited in [citation:4] shows that:

- Entrepreneurs spend more when financing is “0%”

- They take risks they wouldn’t take with cash

Why?

Because the pain of paying is delayed.

The real danger

0% APR doesn’t remove debt.

It postpones the consequences.

Miss the intro deadline and:

- APR jumps to 18–29%

- Interest applies to the remaining balance

- Cash flow tightens instantly

Smart founder rule

If you can’t pay it off during the intro period,

you shouldn’t finance it with a 0% card.

Bonus: A Credit Union Option Worth Knowing

The BrightStar Credit Union Business Elite Rewards card is a lesser-known option:

- 0% APR on purchases for 12 months

- APR starting at 13.49% afterward

- No annual fee

- Limits up to $50,000 [citation:8]

This is a strong option for:

- Local businesses

- Founders with credit union relationships

- Startups seeking lower long-term APR

Final Thoughts

A 0% APR card is not a rewards tool.

It’s a cash-flow strategy.

Used correctly, it:

- Funds growth

- Preserves cash

- Extends your runway

Used incorrectly, it becomes:

- High-interest debt

- A cash-flow trap

- A delayed financial problem

Your startup’s cash flow is your lifeline.

A 0% APR card isn’t free money—it’s a timing tool. Used right, it extends your runway. Used wrong, it’s debt with a delayed fuse. At SmartCardTip.com, we track which issuers are offering the longest intro periods, the highest limits, and the best approval odds for startups in 2026. Compare real-time offers before you apply.

This guide was updated for February 2026 by the SmartCardTip.com team. We analyze dozens of business card offers weekly so startups don’t burn cash on interest.